On October 9, 2025, China's Ministry of Commerce deployed the Foreign Direct Product Rule (FDPR) to rare earth elements for the first time in history. This wasn't merely export quotas or administrative throttling—it was the reverse-engineering of America's most powerful extraterritorial trade weapon, the same mechanism used to cripple Huawei's semiconductor supply chain.

The October 9 announcement introduced provisions scheduled for December 1 implementation that would have required export licenses for any product globally containing ≥0.1% Chinese rare earth content by value, extended controls to products made abroad using Chinese rare earth technologies, and asserted extraterritorial jurisdiction over foreign-produced items through the "50% rule" covering majority-owned affiliates. Legal experts from Mayer Brown, CSIS, Jones Day, and White & Case unanimously characterized this as unprecedented weaponization. As CSIS noted: "The new export controls mark the first time China has applied the foreign direct product rule—a mechanism introduced in 1959 and long used by Washington to restrict semiconductor exports to China."

The sophistication reveals itself in the 0.1% threshold—ten to twenty-five times stricter than U.S. semiconductor de minimis rules of 10-25%. This wasn't amateur retaliation; it was calculated legal engineering designed to capture virtually all global downstream products. Rare earth elements appear in trace amounts throughout modern manufacturing, making the 0.1% threshold effectively omnipresent in enforcement scope.

When Theory Met Reality: The May 2025 Supply Shock

The threat wasn't hypothetical. When China deployed the April 2025 baseline controls—which remain operational today despite the October 30 suspension—supply chains seized with documented consequences. Ford Motor Company shut down its Chicago Assembly Plant for an entire week in late May, with CEO Jim Farley stating on June 13: "It's day to day... We have had to shut down factories. It's hand-to-mouth right now." Similar disruptions hit Suzuki and Maruti production in Japan and India.

The export data confirmed the strategy's effectiveness: China's rare earth magnet exports fell 74% year-over-year in May to 1.2 million kg—the lowest level since February 2020. Exports specifically to the United States dropped 93.3% to only 46,000 kg. The IEA's October 2025 report concluded: "As export volumes fell sharply in April and May, many carmakers in the United States, Europe, and elsewhere struggled to obtain permanent magnets, with some forced to cut utilization rates or even temporarily shut down factories."

July's Prescient Positioning: The Department of Defense Knew

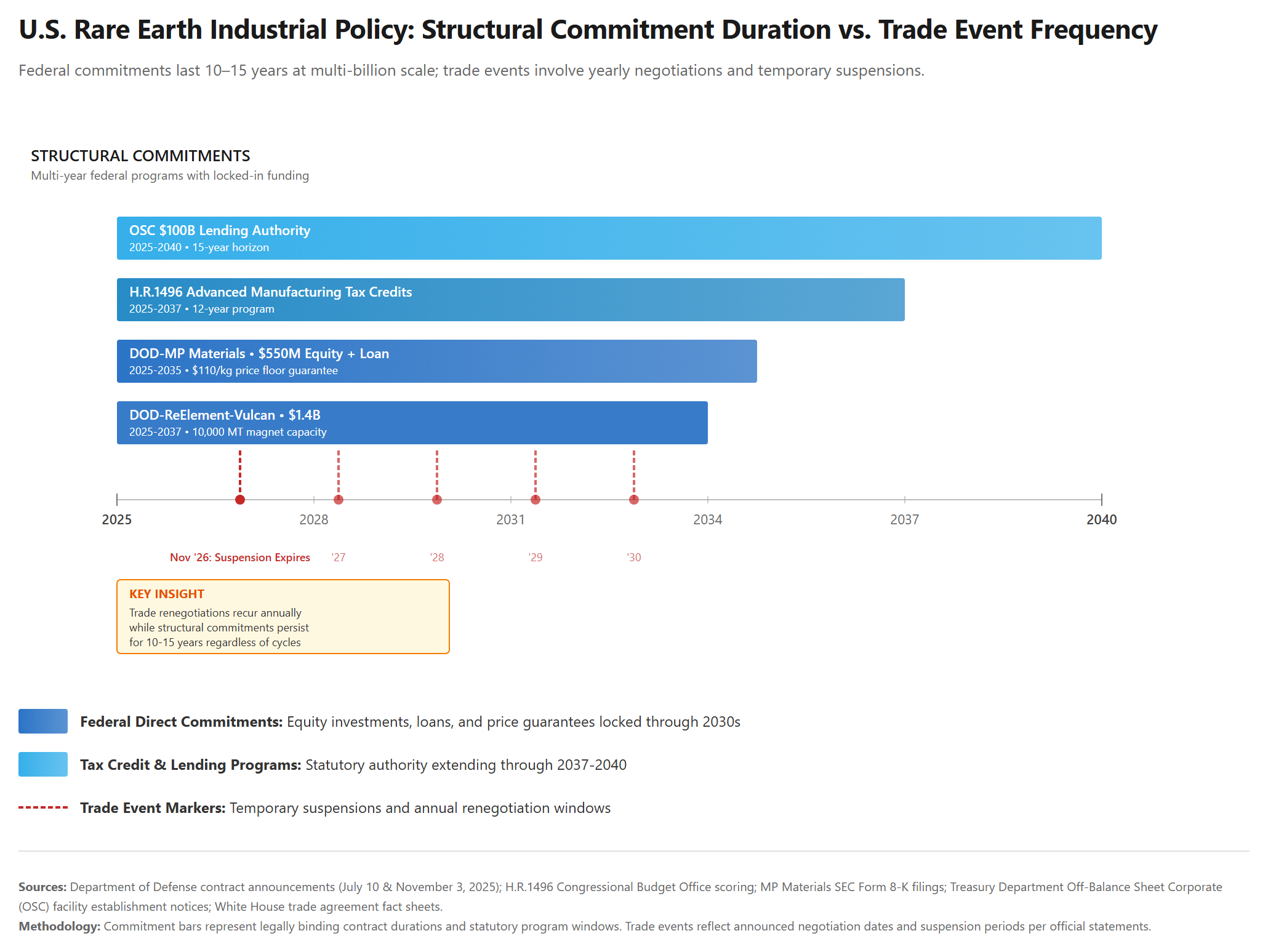

The U.S. government committed over $2 billion to rare earth supply chains in 2025 alone. On July 10, 2025—three months before China's October 9 weaponization—the Department of Defense announced an unprecedented partnership with MP Materials.

The government took a 15% equity stake for $400 million, becoming the company's largest shareholder. More significantly, DOD established a 10-year price floor starting Q4 2025: $110 per kilogram for neodymium-praseodymium oxide, nearly double the ~$60/kg market price at the time.

The structure reveals strategic intent. Through a modified contract-for-difference, DOD commits to pay the difference when market prices fall below $110/kg while receiving 30% of upside above that threshold. At current market prices, this represents an estimated annual cost to DOD of approximately $300 million—sustained expenditure extending through 2035. The deal included an additional $150 million loan and a 10-year offtake agreement for 7,000 metric tons of magnets annually.

This marked the first time the federal government became a major shareholder in a critical minerals company with explicit, decade-long price guarantees. The timing proves this wasn't reactive crisis management—it was intelligence-driven strategic positioning anticipating exactly what materialized on October 9.

The October 30 Deal: Tactical Pause, Strategic Acceleration

Following President Trump's October 30 meeting with Xi Jinping in South Korea, China agreed to suspend the October 9 export control expansion for one year. The White House released detailed terms on November 1, confirming the suspension runs through November 10, 2026, and includes general licenses for rare earths, gallium, germanium, antimony, and graphite.

Critical nuance lost in market celebration: Only the October 9 expansion was suspended. The April 2025 baseline controls on seven rare earth elements—samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium—remain fully operational, requiring export licenses with documented 45-60 day processing delays. While the White House claims general licenses provide "de facto removal" of April controls, Chinese legal documentation and industry reports confirm case-by-case licensing requirements persist, continuing to constrain supply chains.

Treasury Secretary Bessent's post-deal commentary revealed the strategic framework explicitly. When asked what happens after one year, he stated flatly: "We'll be back at the table and we'll get another delay." On using the window: "In the next year or two, we will step away from the sword that China has lifted above us and above the whole world." On China's miscalculation: "China would not be able to pull the same move again... We have offsetting measures."

This isn't hoping for permanent resolution—it's designing a system of managed tension with annual reset points. Each November 2026, 2027, and beyond provides tactical volatility while strategic direction remains fixed toward permanent Western supply chain alternatives.

November 3: Policy Acceleration Despite "Relief"

The ReElement-Vulcan $1.4 billion partnership announced November 3—just days after the trade "relief"—proves the strategic direction unchanged. Funded through the "One Big Beautiful Bill Act" (H.R.1496) providing the Office of Strategic Capital with $100 billion total lending authority, the deal targets 10,000 metric tonnes of NdFeB magnet production capability through vertical integration: ReElement supplies magnet-grade oxides while Vulcan manufactures finished magnets.

Mark Jensen, ReElement CEO: "We are honored to have the support of our government and remain fully committed to meeting the call of our nation." The Department of War receives warrants in ReElement Technologies, maintaining government equity participation established with the MP Materials precedent.

This represents the second major commitment in four months. If the October 30 deal truly resolved the structural vulnerability, why accelerate rather than consolidate? The answer: Government actions speak louder than diplomatic statements. The $110/kg price floor through 2035, the $1.4 billion November partnership, the $100 billion OSC authority, and Congressional H.R.1496 tax credits through 2037 create overlapping commitments that transcend any single administration or annual trade negotiation.

Rare earth stocks crashed on October 27 when trade deal prospects emerged—the same day the S&P 500 rallied on identical news. MP Materials fell 9%, Energy Fuels dropped 14.7%, USA Rare Earth declined 12%, Critical Metals plunged 17%, and Trilogy Metals lost 15%. This paradoxical divergence is definitive proof of investor misunderstanding.

Sophisticated markets don't crash on favorable supply chain developments unless they'd been pricing something incorrectly. The October 27 selloff revealed rare earth investors had positioned for permanent scarcity disruption. When the deal signaled temporary relief, they panic-sold, deflating what they perceived as an overheated "scarcity premium" bubble.

The intraday pattern exhibited classic signs of institutional distribution. MP Materials opened up 3% in premarket trading on October 30 deal confirmation, then closed essentially flat at +0.98%. Volume spiked to 14 million shares versus 9 million average—a 56% increase with $895.66 million in dollar volume traded. High volume on minimal gains followed by immediate reversal: sophisticated money selling into retail enthusiasm.

The Fundamental Disconnect

The market's interpretation was straightforward but wrong: if China eases controls, scarcity premium evaporates, and rare earth stocks should trade on commodity economics rather than strategic value. This logic ignored that MP Materials' $110/kg DOD price floor and 10-year offtake agreement remain unchanged whether China suspends controls for one year or permanently. Government-backed fundamentals are insulated from diplomatic volatility—a distinction the market failed to make on October 27.

The November 3 ReElement announcement confirmed what markets missed: Washington's buildout accelerates regardless of Beijing's tactical concessions. The $1.4 billion commitment wasn't contingent on Chinese export policy remaining restrictive. It was structural, not cyclical.

What the October 27 Selloff Revealed

The market's confusion wasn't random—it exposed a systematic inability to distinguish tactical diplomacy from structural buildout. This pattern will repeat. Every annual November renegotiation through 2035 will generate headlines about "deals" and "truces" that markets will misinterpret as resolution rather than managed tension. The November 3 announcement—$1.4 billion in new commitments arriving 72 hours after markets celebrated relief—already validated this framework.

The opportunity is clear: government-backed price floors and multi-decade commitments are fundamentally insulated from twelve-month diplomatic cycles. Markets that sell relief while governments accelerate commitments aren't pricing risk—they're creating it for those who mistake noise for signal.

The October 27 paradox—rare earth stocks crashing while the S&P rallied on identical trade news—revealed fundamental investor misunderstanding. Markets priced the sector for permanent disruption, then panic-sold on temporary relief. Treasury Secretary Bessent's explicit framing of annual renegotiations as permanent framework removes all ambiguity: this isn't cyclical trade war noise, it's structural transformation with multi-decade government commitments.

Investment differentiation matters more than sector-wide exposure. Tier 1 (Government-Backed): MP Materials' $110/kg DOD price floor through 2035 eliminates catastrophic downside while preserving upside participation; ReElement-Vulcan's $1.4B Department of War partnership with warrants follows the same de-risked pattern. Tier 2 (Commercial Scale): Energy Fuels and Lynas offer pure scarcity premium exposure without government backing—higher beta to sector dynamics but vulnerable to Chinese price suppression. Tier 3 (Development Stage): USA Rare Earth (H1 2026 Oklahoma facility) and Ucore (Pentagon Phase 2 funding) carry binary execution risk with asymmetric upside if government support expands.

China's multi-track approach revealed itself before the rare earth deal was even finalized. On October 26—four days before the October 30 "truce"—China announced export controls on silver, antimony, and tungsten for 2026-27 (MOFCOM Announcement No. 68). These restrictions cover minerals where China maintains similar dominance (80% of global tungsten supply). The simultaneity matters: China negotiated the rare earth suspension while tightening controls on adjacent critical minerals. This validates the core thesis: tactical pauses on specific commodities do not represent strategic resolution of supply chain weaponization.

November 10, 2026 expiration represents the first test of the Bessent Doctrine. Markets will begin pricing this as early as March-May 2026, with peak uncertainty in September-October 2026—expect recurring volatility every spring as annual deadlines approach. Most critically: Watch whether MP Materials' 10X Facility (10,000 MT magnet capacity) remains on schedule for 2028 commissioning. That milestone represents the inflection point where Western capacity moves from symbolic to material—reaching approximately 15-20% of non-Chinese global demand. Until then, managed tension and annual renegotiation remain the strategic reality.

China's October 9 FDPR deployment represents unprecedented sophistication in economic coercion—reverse-engineering America's most powerful extraterritorial trade weapon and deploying it where China holds 90% leverage versus U.S. 20% semiconductor share. The evidence for permanent structural shift is overwhelming: $2 billion U.S. commitments in 2025, price floors through 2035, Congressional tax credits through 2037, and $100 billion OSC lending authority. The November 3 announcement just days after "relief" proves policy acceleration, not consolidation. The 2.0-point deduction accounts for execution risks: timeline gaps between November 2026 expiration and 2028 Western capacity creates tactical vulnerability requiring annual diplomatic management. May 2025 supply disruptions (Ford shutdowns, 74% export collapse) prove the threat operational. The October 27 market paradox provides documented evidence of investor misunderstanding.

This commentary is provided for informational purposes only and does not constitute investment advice, an offer to sell, or a solicitation to buy any security. The information presented represents the opinions of The Stanley Laman Group as of the date of publication and is subject to change without notice.

The securities, strategies, and investment themes discussed may not be suitable for all investors. Investors should conduct their own research and due diligence and should seek the advice of a qualified investment advisor before making any investment decisions. The Stanley Laman Group and its affiliates may hold positions in securities mentioned in this commentary.

Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal. Forward-looking statements, projections, and hypothetical scenarios are inherently uncertain and actual results may differ materially from expectations.

The information contained herein is believed to be accurate but is not guaranteed. Sources are cited where appropriate, but The Stanley Laman Group makes no representation as to the accuracy or completeness of third-party information.

This material may not be reproduced or distributed without the express written consent of The Stanley Laman Group.

© 2025 The Stanley-Laman Group, Ltd. All rights reserved.

SLG is an independent investment management and advisory firm serving ultra-high-net-worth individuals, families, and institutions.