On October 23, Texas regulators quietly approved permits for 210 industrial natural-gas generators in Shackelford County, a rural stretch roughly forty minutes from Abilene. The application, filed by Voltagrid on behalf of Oracle and OpenAI, confirmed that the second Project Stargate data-center campus will operate entirely behind the meter—generating its own 1.4 gigawatts of power rather than waiting years for a grid connection.

This isn't a backup plan; it's the new playbook.

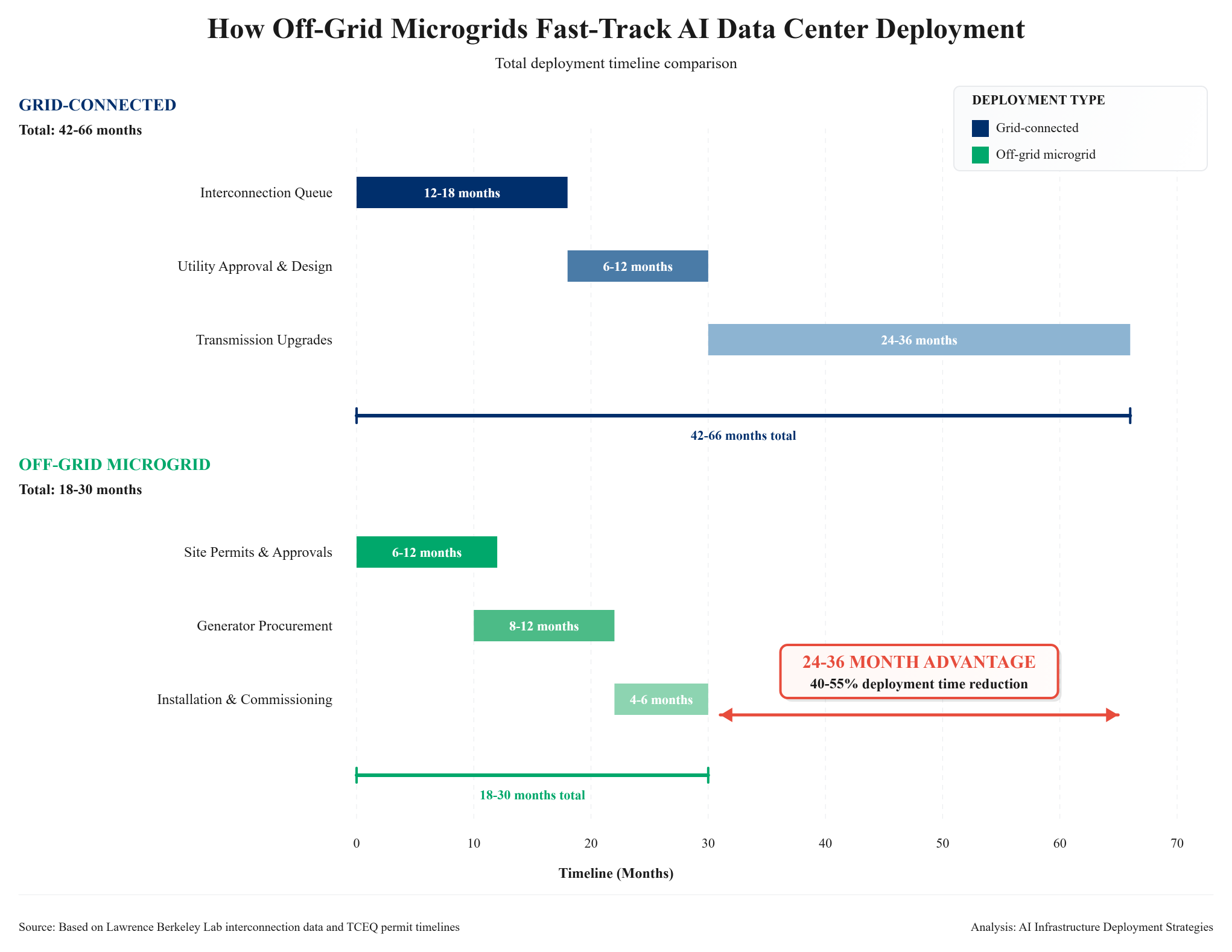

The economics are extreme but strategically rational. Traditional grid-connected data centers invest about $250–450 million per gigawatt for interconnection infrastructure. Oracle's off-grid facility requires roughly $1.3–2.1 billion per gigawatt—a 3–5x capital premium—plus 50–75% higher annual operating costs ($470–920 million versus $280–560 million for grid power). In effect, Oracle is paying several multiples of traditional cost to accelerate deployment by 18–24 months—cutting a typical 42–66 month grid-connection timeline nearly in half.

This willingness to absorb such a premium validates the underlying economics: AI infrastructure generates returns that justify 3–5x premiums for speed. Rational actors don't pay $1.4 billion extra for speculation—they pay it because deployment delay destroys more value than the premium costs. This project's cost structure validates that the AI buildout is durable, not ephemeral.

At 197 primary Jenbacher units and 13 backups, the system ranks among the largest private power deployments in U.S. history. More important, it exposes the real constraint on AI infrastructure: not capital, not chips, but electrons—and the multi-year timelines needed to access them through conventional utilities.

Oracle isn't alone in this calculation. Elon Musk's xAI Memphis facility already operates on natural gas microgrids, with plans for a private 1 GW plant in Mississippi. Meta's Louisiana data center—initially projected to strain the state grid with $3 billion in utility infrastructure needs—is evaluating hybrid approaches. Even companies pursuing long-term nuclear strategies are testing near-term gas solutions as operational bridges.

The Shackelford permits also reveal why this strategy can't scale everywhere. It works in West Texas because of Permian Basin gas infrastructure and a permitting environment that approved the project in under six months. The region's existing pipeline network—built to serve the Permian's oil and gas production—can deliver the 12 million cubic feet of natural gas daily that 210 generators require, infrastructure that would take 2-4 years to build in other markets. Replicating it in Northern Virginia—the nation's largest data-center market—would confront gas-pipeline congestion and multi-year environmental reviews. In Washington, Oregon, and California, fossil-fuel generation faces political and regulatory barriers that make such projects virtually impossible.

Realistic off-grid penetration tops out around 15–25% of total U.S. AI-data-center capacity through 2027, concentrated in gas-rich states: Texas (5–8 GW), Louisiana (2–3 GW), and Pennsylvania-Ohio (2–3 GW). The remaining 75–85% will still rely on utility grids, meaning the power constraint persists—just partially alleviated for first-movers willing to pay premium costs in favorable jurisdictions.

The investment ripple reaches far beyond the grid. Off-grid deployment could lift effective AI capacity to 22–27 GW by 2027—nearly double what a grid-only path allows—turning a potential 50% shortfall into a fraction of that. This extended buildout keeps semiconductor demand alive for 4–5 years rather than creating a two-year surge-and-slump. The bottleneck hasn't vanished—it's been redistributed across time, creating steadier earnings visibility rather than the feared 2026 cliff.

If you followed this week's headlines, AI's power crisis appeared solved. The U.S. government committed $80 billion to Westinghouse reactors. Microsoft finalized plans to restart Three Mile Island. Google and Amazon announced small modular reactor partnerships with Kairos Power and X-energy. Media coverage framed nuclear as the carbon-free infrastructure breakthrough the industry desperately needed.

There's one problem: none of those electrons arrive before 2030.

The issue isn't the technology—it's the timeline. Small modular reactors from Kairos and X-energy target commercial operation between 2030 and 2035, and even industry observers call those projections "very optimistic." Full-scale AP1000 reactors face even longer horizons. The Westinghouse reactors at Georgia's Vogtle plant—the only U.S. nuclear units completed this century—began construction on March 15, 2013 and didn't reach commercial operation until July 2023 and April 2024: a 10-11 year build cycle, seven years behind schedule, with costs exploding from $14 billion to $34 billion. This pattern makes corporate planning around nuclear timelines essentially impossible.

AI data centers need power in 2026-2027, not the early 2030s. Hyperscalers are deploying hundreds of billions in GPU clusters and facility construction over the next 24-36 months. Nuclear solves a 2030s constraint while doing nothing for the immediate bottleneck that forced Oracle to install 210 gas generators in Texas.

This creates a deployable hierarchy:

Ironically, renewable energy faces the same constraint. Lawrence Berkeley Lab reports 2.6 terawatts stuck in interconnection queues—twice America's entire generation capacity. Solar and wind projects wait in the same line as data centers, making renewables equally unavailable on AI's 2026-2027 timeline.

The nuclear announcements serve a different strategic purpose. They demonstrate long-term commitment to sustained AI infrastructure investment while providing political cover for near-term fossil fuel solutions. Oracle can install 210 gas generators today while announcing plans to transition to Westinghouse reactors in 2035—a timeline that satisfies ESG commitments without delaying deployment. "We're going nuclear eventually" makes it easier to justify "we're using natural gas now."

For capital allocation through 2027, the hierarchy is clear: natural gas infrastructure, generator manufacturers, and microgrid developers are the cash-flow plays. Nuclear plays—whether reactor restarts, SMR developers, or uranium suppliers—represent valid multi-year themes requiring patience through regulatory approvals and construction timelines extending into the 2030s. Both pathways address the same constraint across different timeframes.

The Shackelford County microgrid crystallizes AI infrastructure's binding constraint: not capital or compute, but megawatts and the timeline to access them. Oracle's willingness to pay 4x premiums validates that deployment speed destroys more value than extreme costs—this is revealed preference with $2 billion at stake.

Off-grid solutions address 15-25% of the power bottleneck through 2027, concentrated where gas infrastructure and permitting align: Texas (5-8 GW), Louisiana (2-3 GW), Pennsylvania-Ohio (2-3 GW). This transforms a potential 50% capacity shortfall into a manageable delay, extending the semiconductor cycle through 2027-2028 rather than creating a 2026 cliff.

Meanwhile, nuclear announcements provide strategic positioning and political cover—even as residential ratepayers face $16-18 monthly increases to fund the same infrastructure hyperscalers bypass. The deployment hierarchy is clear: gas microgrids for 2026-2027 needs, reactor restarts for late-cycle capacity, SMRs for the 2030s.

Geographic arbitrage becomes the investment reality. Data center REITs with Texas exposure gain structural advantages. Pipeline operators, generator manufacturers (Jenbacher/Wärtsilä), and microgrid developers represent near-term cash flows, with Kinder Morgan and Energy Transfer already seeing pipeline capacity inquiries from data center developers. Nuclear plays—SMR developers, uranium miners, reactor restarts—offer valid multi-year exposure requiring patience through 2030+.

Watch capital allocation, not press releases. Companies building private power plants believe in AI economics more than those merely announcing nuclear partnerships.

The Shackelford County microgrid represents genuine structural adaptation with clear investment implications. Verified regulatory filings, quantifiable economics ($2B for 1.4 GW), and immediate deployment impact (2026 vs. 2029) make this one of the clearest signals of Q4 2025. The rating reflects both the signal's strength and its inherent limitations: this solution addresses only 15-25% of the constraint and works only in specific geographies with gas infrastructure and favorable permitting. Nevertheless, the willingness to pay 4x premiums validates AI infrastructure economics more powerfully than any earnings call could. This signal reveals not just what companies are building, but what they're willing to pay to build it—and that price discovery itself is the story.

This commentary is provided for informational purposes only and does not constitute investment advice, an offer to sell, or a solicitation to buy any security. The information presented represents the opinions of The Stanley Laman Group as of the date of publication and is subject to change without notice.

The securities, strategies, and investment themes discussed may not be suitable for all investors. Investors should conduct their own research and due diligence and should seek the advice of a qualified investment advisor before making any investment decisions. The Stanley Laman Group and its affiliates may hold positions in securities mentioned in this commentary.

Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal. Forward-looking statements, projections, and hypothetical scenarios are inherently uncertain and actual results may differ materially from expectations.

The information contained herein is believed to be accurate but is not guaranteed. Sources are cited where appropriate, but The Stanley Laman Group makes no representation as to the accuracy or completeness of third-party information.

This material may not be reproduced or distributed without the express written consent of The Stanley Laman Group.

© 2025 The Stanley-Laman Group, Ltd. All rights reserved.

SLG is an independent investment management and advisory firm serving ultra-high-net-worth individuals, families, and institutions.