Amazon launched Rufus—its generative AI shopping assistant—in February 2024. By Black Friday 2025, it had become something more significant than a product feature: conversion infrastructure operating at scale.

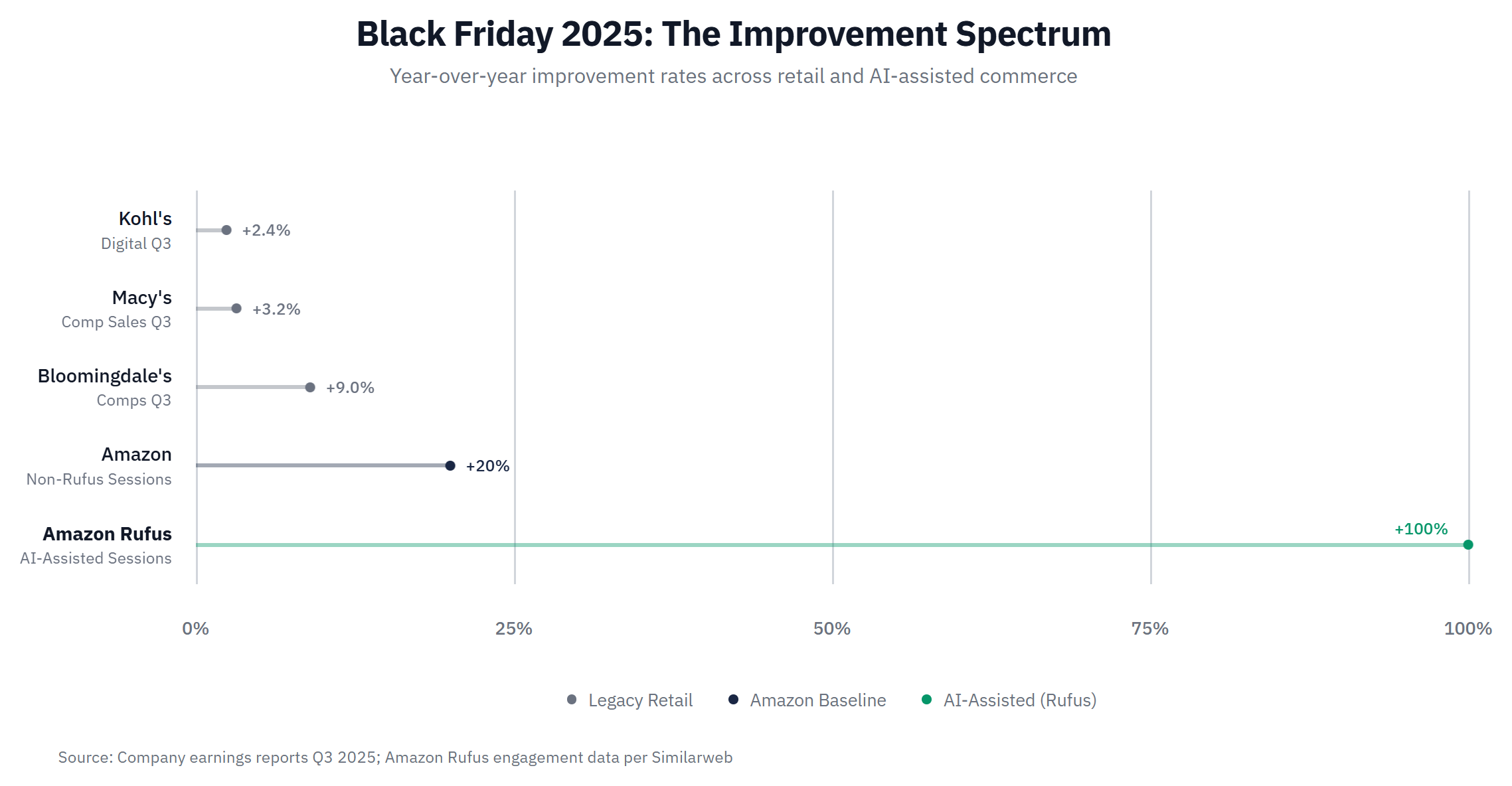

Sensor Tower's post-holiday analysis revealed that 40% of Amazon mobile app sessions on Black Friday engaged Rufus, up from approximately 30% in early November. The conversion numbers mattered more: sessions using Rufus showed a 100% increase in conversion rates compared to the trailing 30-day average. Sessions without Rufus improved by just 20%. The 5x differential isn't marginal. It's structural.

On the Q3 earnings call, CEO Andy Jassy said he expects Rufus to generate more than $10 billion in incremental annual sales. That estimate now looks conservative given Black Friday's performance. Over 250 million customers used Rufus in 2025, with monthly active users up 140% year-over-year and total interactions up 210%.

The mechanism is efficiency. Rufus users showed 60% higher purchase completion rates overall, reflecting faster decisions, higher confidence, and elevated average order values. The AI reduces friction at precisely the moments that typically cause mobile abandonment—product comparison, specification questions, compatibility concerns.

This matters because mobile commerce faces a persistent structural problem: conversion rates remain roughly half those of desktop. Industry benchmarks consistently show desktop converting at 2x the mobile rate, despite mobile capturing 54-56% of Black Friday sales and 70-80% of traffic. Retailers have spent years optimizing checkout flows, reducing page load times, and simplifying forms. The gap hasn't closed.

Traditional mobile optimization delivers linear improvement—faster loading, smoother checkout, cleaner design. These investments yield single-digit conversion gains at substantial cost. AI shopping assistants appear to operate differently: by integrating with catalog data, purchase history, and recommendation engines, they address the fundamental discovery and decision friction that mobile UX optimization never solved.

The Rufus data illuminates the difference between linear and multiplicative improvement.

Consider the comparison: Macy's invested heavily in its "Bold New Chapter" strategy—store closures, luxury focus through Bloomingdale's, operational efficiency. The result was Q3 comparable sales of +3.2%, its strongest quarter in more than three years. That's genuine progress. Kohl's hired a new Chief Digital Officer in July, restructured its app team, and improved digital sales from -7.7% in Q1 to +2.4% in Q3. That, too, is genuine progress.

But +3.2% through traditional execution and +100% through AI infrastructure aren't competing on the same scale. Amazon didn't improve its conversion by 100%—it improved Rufus-assisted conversion by 100% while non-Rufus conversion improved by only 20%. The infrastructure advantage compounds on itself.

The concentration effect extends beyond Amazon's own AI. Apptopia data shows ChatGPT shopping referrals rose 28% year-over-year over the Black Friday weekend, but Amazon captured 54% of those referrals—up from 40% in 2024. AI isn't democratizing commerce; it's accelerating concentration toward platforms with structured, parseable inventory data.

The pattern holds across the industry. Adobe Analytics reported that AI traffic to retail sites grew 805% year-over-year, with AI-referred shoppers 38% more likely to convert than organic visitors. Shopify merchants generated $6.2 billion on Black Friday (+25% YoY) with Shop Pay processing 32% of all orders. The platform model creates aligned incentives: Shopify earns more when its merchants sell more, driving continuous investment in conversion infrastructure.

The CapEx differential makes the gap durable. Walmart projects $20–25 billion in annual capital expenditure, with significant allocation to AI and supply chain automation. Macy's is guiding to well under $1 billion. An order-of-magnitude spending gap can't be closed through efficiency—it would require strategic transformation that department store balance sheets can't fund.

Kohl's Q3 improvement deserves acknowledgment—the new CDO appears to be having an impact. But the company has announced no AI shopping assistant, no technology platform partnerships, and no CapEx expansion. Incremental digital improvement while competitors deploy AI that doubles conversion isn't catching up. It's falling further behind at a slower rate.

The Q3 earnings cycle delivered what department store bulls had been waiting for. Macy's posted comparable sales of +3.2%, its best performance in thirteen quarters. Bloomingdale's comparable sales surged 9%. Kohl's digital sales swung from -7.7% in Q1 to +2.4% in Q3. CFO Jill Timm told investors that traffic improved from "high single digits in August to high teens in October." The turnaround narrative, which had grown stale through quarters of decline, suddenly had momentum.

Black Friday foot traffic data introduced a complication. On Black Friday, Kohl's declined 5.3%, Macy's fell 5.9%, and JCPenney dropped 6.7%. The weather excuse melts under scrutiny. While department store anchors fell 5-6%, traffic to indoor malls actually rose +3.1%. Shoppers braved the storm for Apple, Sephora, and the food court—they bypassed the anchors. Management will point to the Midwest blizzard—which dropped 8.4 inches on Chicago on Saturday, November 29, driving regional traffic down 35-41%. Fair enough. But Kohl's is headquartered in Wisconsin and concentrated in the Midwest. That geographic exposure to weather disruption isn't temporary; it's structural.

The deeper issue is what the turnaround metrics don't address: the highest-margin component of the department store business model is degrading faster than merchandise sales are recovering.

The structural shift is clearer in customer acquisition than revenue. New store credit card account openings have fallen in seven of the past eight years, according to Equifax—younger shoppers increasingly opt for buy-now-pay-later instead. While Macy's credit revenue has recovered from a 2023 delinquency crisis (+32% in Q3 2025), that recovery came from higher APRs and tightened underwriting, not portfolio growth. BNPL's $747 million Black Friday represents the next generation's preferred payment infrastructure—one that routes around traditional retail credit entirely.

Shop Pay Installments (powered by Affirm) is integrated into 32% of Shopify orders. Klarna, Afterpay, and similar products appear prominently at checkout across the ecommerce landscape—capturing the financing relationship at the exact moment of highest purchase intent.

The CFPB's late fee cap—reducing maximum fees from $32 to $8—further erodes store card economics.

Credit stress is intensifying—41% of BNPL users have missed a payment in 2025, up from 34% in 2024. Bad debt assumptions are rising. Delinquencies are accelerating. CFO Adrian Mitchell acknowledged that "rising delinquencies contribute to increased bad debt" that offsets interest rate benefits.

This is the second-order effect the turnaround narrative ignores. Macy's can stabilize merchandise comparable sales through better assortment, fewer stores, and improved execution. But recovering revenue from a shrinking customer base isn't the same as building a durable credit franchise. The next generation's payment preferences are already locked in.

Celebrating +3.2% comps while ignoring the generational shift in payment infrastructure is like celebrating temperature stabilization while the foundation cracks.

Black Friday revealed a retail industry where improvement and competitive position have decoupled.

Macy's posted its best quarter in thirteen quarters. Kohl's digital turned positive. But Rufus demonstrating 100% conversion lift at 40% penetration shows what multiplicative improvement looks like. Department stores are getting 3% better. Platforms are deploying infrastructure that doubles conversion rates.

The investment implications follow the rate of improvement, not the direction. Amazon and Shopify are long positions not because department stores are failing—they're not—but because AI-driven conversion infrastructure compounds advantages faster than traditional retail execution can close them. The $10 billion incremental revenue estimate from Jassy has Black Friday validation.

The short thesis on department stores strengthened despite improved Q3 metrics. Credit card account acquisition—which fuels the high-margin financing business—has declined seven of the past eight years as BNPL and Shop Pay capture the next generation's payment preferences. Even if merchandise comps stabilize, the customer acquisition engine is broken—and with it, the path to rebuilding a high-margin credit franchise. This is franchise erosion that doesn't appear in comparable sales figures.

Retail isn't bifurcating into digital versus physical. It's bifurcating into utility versus discovery. Amazon wins utility—customers know what they want and expect frictionless acquisition. Off-price retailers win discovery—customers want treasure-hunt serendipity and value. Department stores are optimized for neither. They can't match Amazon on utility infrastructure. They can't match TJ Maxx on discovery and value. The positioning failure is more fundamental than the technology gap.

Watch Q4 earnings for two metrics: credit card revenue in the "Other Income" line, and any AI shopping assistant announcements from Walmart or Target. The next data points will confirm or challenge whether Rufus represents Amazon's unique advantage or the beginning of a broader AI-driven restructuring of retail conversion economics.

First empirical proof at scale that AI shopping assistants drive multiplicative conversion improvement. The 100% lift versus 20% for non-Rufus sessions isn't marginal—it's structural. The 40% penetration rate on Black Friday shows mainstream adoption, not early-adopter novelty.

Rated 8.1 rather than 9+ for three reasons: this is one holiday from one retailer requiring Q4/Q1 confirmation; conversion lift may partially reflect self-selection as higher-intent shoppers gravitate toward Rufus; and competitor AI responses from Walmart and Target aren't yet visible. One caveat on platform concentration: Shopify experienced partial admin dashboard latency on Cyber Monday—a reminder that infrastructure reliance introduces single-point-of-failure risk, even as aggregate volume remained robust.

The credit card finding amplifies the thesis—even recovering credit revenue doesn't address the structural erosion of account acquisition. New store card openings have declined seven of the past eight years. This creates an asymmetric information opportunity: investors seeing +3.2% comps may miss the generational payment shift that matters more to long-term franchise value.

This commentary is provided for informational purposes only and does not constitute investment advice, an offer to sell, or a solicitation to buy any security. The information presented represents the opinions of The Stanley Laman Group as of the date of publication and is subject to change without notice.

The securities, strategies, and investment themes discussed may not be suitable for all investors. Investors should conduct their own research and due diligence and should seek the advice of a qualified investment advisor before making any investment decisions. The Stanley Laman Group and its affiliates may hold positions in securities mentioned in this commentary.

Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal. Forward-looking statements, projections, and hypothetical scenarios are inherently uncertain and actual results may differ materially from expectations.

The information contained herein is believed to be accurate but is not guaranteed. Sources are cited where appropriate, but The Stanley Laman Group makes no representation as to the accuracy or completeness of third-party information.

This material may not be reproduced or distributed without the express written consent of The Stanley Laman Group.

© 2025 The Stanley-Laman Group, Ltd. All rights reserved.

SLG is an independent investment management and advisory firm serving ultra-high-net-worth individuals, families, and institutions.