Here's the simplest way to understand what's happening: imagine building a supercomputer the size of a credit card. Physics won't let you make one giant chip—the manufacturing yields collapse. Instead, you make several smaller chips and connect them with microscopic wires thinner than a human hair. The machines that do this stitching are in desperately short supply.

TSMC, the company that manufactures chips for Nvidia, Apple, and AMD, has a packaging technology called CoWoS (Chip-on-Wafer-on-Substrate). Every Nvidia Blackwell GPU—the chips powering the AI boom—requires CoWoS packaging. The problem is straightforward: TSMC cannot build CoWoS capacity fast enough to meet demand.

On December 8, UBS analyst S. Lin raised demand forecasts across the board. Nvidia's CoWoS demand for 2025-26 was revised upward by 10% and 8% respectively, driven by higher Blackwell production volumes. AMD's 2026 forecast jumped 23%, reflecting larger package designs for MI400 accelerators—with related wafer demand expected to grow 83% year-over-year. Amazon's Trainium is projected to double its CoWoS wafer demand in 2026. Broadcom's TPU demand rises 51%. The gap between what customers want and what TSMC can deliver isn't closing—it's widening.

UBS expects TSMC to expand monthly CoWoS capacity from approximately 70,000 wafers to 100,000 by end of 2026—a 43% increase in a single year. Total GPUs using CoWoS packaging will rise from 6.1 million to 6.7 million units. And this expansion is backed by real money: investment in cloud AI by US hyperscalers is projected to grow 62% in 2025 alone.

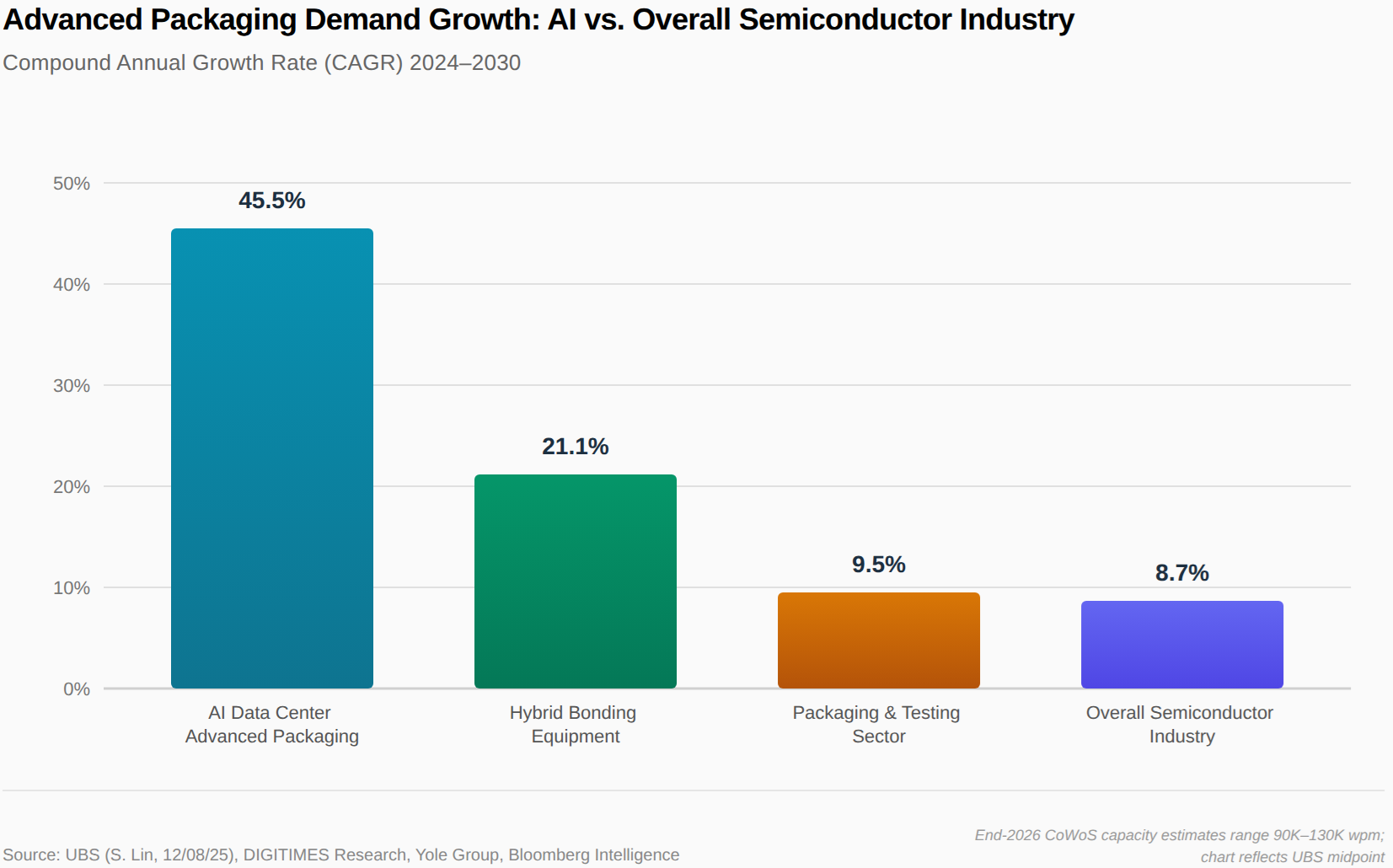

The numbers tell a story that cuts against the prevailing narrative. According to DIGITIMES Research, advanced packaging specifically for AI data center chips is growing at 45.5% annually through 2030. This AI-specific segment is growing five times faster than the overall semiconductor industry's 8.7% growth rate. Bloomberg Intelligence projects the total advanced packaging market could reach $80 billion by 2033.

What makes this different from typical semiconductor cycles is the customer base. Traditional chip packaging serves consumer electronics companies managing quarterly inventory. Advanced packaging serves hyperscalers making multi-year infrastructure commitments. These customers don't cancel orders when stock prices dip.

The next constraint is already visible. As chips grow more complex, the industry is moving toward hybrid bonding—a technology that fuses copper surfaces directly together, atom to atom. Instead of using tiny metal bumps to connect chips, hybrid bonding allows chips to be stacked vertically, dramatically increasing performance while reducing power consumption.

The technology transition creates a strategic divergence worth understanding. Samsung has stated publicly that hybrid bonding is "essential" for next-generation 16-stack memory chips launching in 2026—they need the technology leap to compete. SK Hynix, the current market leader, is taking a different path: extending its proprietary MR-MUF technology while developing hybrid bonding as a "parallel track" for higher-density products in 2027-2028. Either way, billions in equipment spending flows.

The machines that perform hybrid bonding are made by a handful of companies. The market leader is a Dutch company most investors have never heard of: BE Semiconductor Industries, known as BESI. Its hybrid bonding systems are already qualified at TSMC, Samsung, and the major memory manufacturers. In April 2025, Applied Materials—the world's largest semiconductor equipment maker—acquired a 9% stake in BESI, creating an integrated front-end to back-end workflow that validates the technology's strategic importance.

BESI's positioning is unusually defensible. Hybrid bonding equipment revenue is projected to grow from $152 million in 2025 to $397 million by 2030—a 21% compound annual growth rate. The company has visibility into hybrid bonding programs extending through 2028. Orders last quarter rose 36.5% sequentially—even as revenue declined 15% year-over-year. That divergence is the classic "bottom of cycle" signal: orders leading, revenue lagging.

This matters because BESI isn't a bet on whether AI continues. It's a bet on whether AI chips require assembly—which they do, by definition. Every Nvidia GPU, every AMD accelerator, every custom chip from Amazon or Google must pass through advanced packaging. The company sits at a chokepoint that exists regardless of which AI chip designer wins market share.

TSMC's planned capacity expansion means someone has to build the equipment. That demand is now visible through 2028.

Semiconductor equipment follows predictable boom-bust cycles. This is the pattern investors have observed for decades: equipment makers surge during buildout phases, then collapse when capacity catches up with demand. After the 2021-2022 surge, inventory corrections hit the industry. Smartphone sales remain sluggish. Automotive chip demand softened. BESI's own revenue was down 15% year-over-year last quarter.

Classic late-cycle warning signs, right? The bears argue we're approaching that inflection point—the moment when capacity catches demand and equipment orders fall off a cliff. They point to historical patterns and argue that this cycle is no different. And in fairness, they're not entirely wrong about the legacy segments.

Traditional chip packaging—the kind used for smartphones and laptops—is indeed cyclical. When Apple sells fewer iPhones, packaging equipment demand falls. When automotive production slows, orders decline. BESI's legacy business in these markets, which still represents roughly 60% of revenue, is genuinely soft. This is the world the bears are pattern-matching to, and within that world, their caution is reasonable.

But advanced packaging for AI chips operates on different logic entirely. The customers are different: hyperscalers making decade-long infrastructure commitments rather than consumer electronics companies managing quarterly inventory. The capacity commitments are different: Nvidia has booked production slots through 2028, and Amazon's Trainium chips are ramping on contracted schedules. When TSMC builds a new packaging facility, the equipment orders are backed by customer commitments, not speculative forecasts.

The technology transition is different. Hybrid bonding isn't an incremental upgrade—it's a prerequisite for next-generation chip architectures. Samsung needs it to compete in high-bandwidth memory. TSMC needs it for advanced logic integration. This isn't optional demand that disappears in a downturn.

What the cyclical framework misses is what happened December 8. UBS didn't lower forecasts—they raised them. Across the board: Nvidia, AMD, Amazon, Broadcom. Cloud AI investment up 62%. This isn't what cyclical peaks look like.

BESI's Q3 orders rose 36.5% sequentially while revenue declined 15%. That divergence matters: in semiconductor equipment, orders are the leading indicator, revenue the lagging one. The bears see the revenue decline and pattern-match to historical downturns. They're missing that orders are pointing in the opposite direction.

The pattern recognition that served investors well in previous semiconductor cycles is now creating a blind spot. The equipment demand for AI packaging isn't following the consumer electronics playbook because the underlying customers—and their capital commitment structures—are fundamentally different.

There's a credible bear case here, but it requires believing that AI infrastructure spending collapses before the packaging buildout completes. Given hyperscaler capital expenditure commitments exceeding $350 billion in 2025 alone, that's a specific bet against companies that have demonstrated extraordinary willingness to invest.

The bears are applying a framework built for consumer electronics to a constraint defined by enterprise infrastructure. The two markets have different customers, different commitment structures, and different cycle dynamics.

The AI infrastructure buildout has moved through sequential bottlenecks. In 2023, the constraint was GPU availability—Nvidia couldn't fabricate chips fast enough. In 2024, it was high-bandwidth memory—HBM was allocated years in advance. In 2025 and 2026, the constraint is shifting to packaging.

Each bottleneck creates pricing power and demand visibility for the companies that solve it. Nvidia's margins expanded when GPUs were scarce. Memory makers SK Hynix and Micron saw profits surge when HBM tightened. The same dynamic is now emerging in packaging equipment.

The Signal (packaging bottleneck intensifying) directly contradicts the Noise (equipment cycle peaking). Both cannot be true. The December 8 UBS revisions—every major customer's demand raised, 62% cloud AI investment growth, 6.7 million GPUs requiring CoWoS—suggest the Signal is winning.

For investors who believe AI infrastructure spending continues, BESI represents exposure to a chokepoint that every AI chip must pass through. The company trades at a premium valuation, but the market may be underestimating how long the equipment cycle extends when the constraint is structural rather than cyclical.

The key variable to watch is Samsung versus SK Hynix technology choices. Samsung's aggressive hybrid bonding adoption drives near-term equipment demand. If SK Hynix successfully extends its MR-MUF technology, the hybrid bonding inflection shifts later—but doesn't disappear. Either path generates equipment spending; only the timing differs.

Watch Q1 2026 equipment orders. If the cyclical thesis were correct, orders would be decelerating. If the structural thesis holds, TSMC's capacity expansion will translate into sustained equipment demand that extends well beyond what current valuations reflect. The constraint dictates the opportunity—and the constraint isn't breaking.

Advanced packaging represents a genuine, measurable constraint on AI chip deployment. The December 8 UBS report provides institutional-grade validation: demand forecasts raised across Nvidia (+10%), AMD (+23%), Amazon (doubling), Broadcom (+51%), with US cloud AI investment projected to grow 62% in 2025. BESI's Q3 order surge (up 36.5% while revenue declined) confirms the cycle turn. The Applied Materials 9% stake validates BESI's technology leadership.

Rated 8.0 rather than higher because timing uncertainty remains material. SK Hynix's decision to extend MR-MUF technology rather than immediately adopting hybrid bonding could push the hybrid bonding volume inflection from 2026 toward 2027-2028. BESI is still exposed to broader semiconductor sentiment regardless of structural differentiation. Competition from ASMPT introduces execution risk.

The signal is strong and now institutionally validated. The timing of when hybrid bonding specifically becomes dominant remains the key uncertainty.

This commentary is provided for informational purposes only and does not constitute investment advice, an offer to sell, or a solicitation to buy any security. The information presented represents the opinions of The Stanley Laman Group as of the date of publication and is subject to change without notice.

The securities, strategies, and investment themes discussed may not be suitable for all investors. Investors should conduct their own research and due diligence and should seek the advice of a qualified investment advisor before making any investment decisions. The Stanley Laman Group and its affiliates may hold positions in securities mentioned in this commentary.

Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal. Forward-looking statements, projections, and hypothetical scenarios are inherently uncertain and actual results may differ materially from expectations.

The information contained herein is believed to be accurate but is not guaranteed. Sources are cited where appropriate, but The Stanley Laman Group makes no representation as to the accuracy or completeness of third-party information.

This material may not be reproduced or distributed without the express written consent of The Stanley Laman Group.

© 2025 The Stanley-Laman Group, Ltd. All rights reserved.

SLG is an independent investment management and advisory firm serving ultra-high-net-worth individuals, families, and institutions.