For thirty years, FAR Part 31 has functioned as the defense industry's most effective barrier to entry. The regulation governs cost allowability for government contracts, requiring contractors to maintain segregated cost pools, submit to Defense Contract Audit Agency examinations, and operate government-approved business systems across estimating, accounting, purchasing, material management, earned value, and property. Building this infrastructure costs hundreds of millions annually. Lockheed Martin's G&A rate approaches 8% of revenue—partially driven by these government-unique compliance burdens.

Commercial software companies accustomed to 80% gross margins couldn't justify this investment for speculative defense revenue. The compliance infrastructure acted as a moat, protecting incumbent primes from competition in precisely the domains where commercial technology has surpassed military-specific development: software, artificial intelligence, sensors, and data analytics.

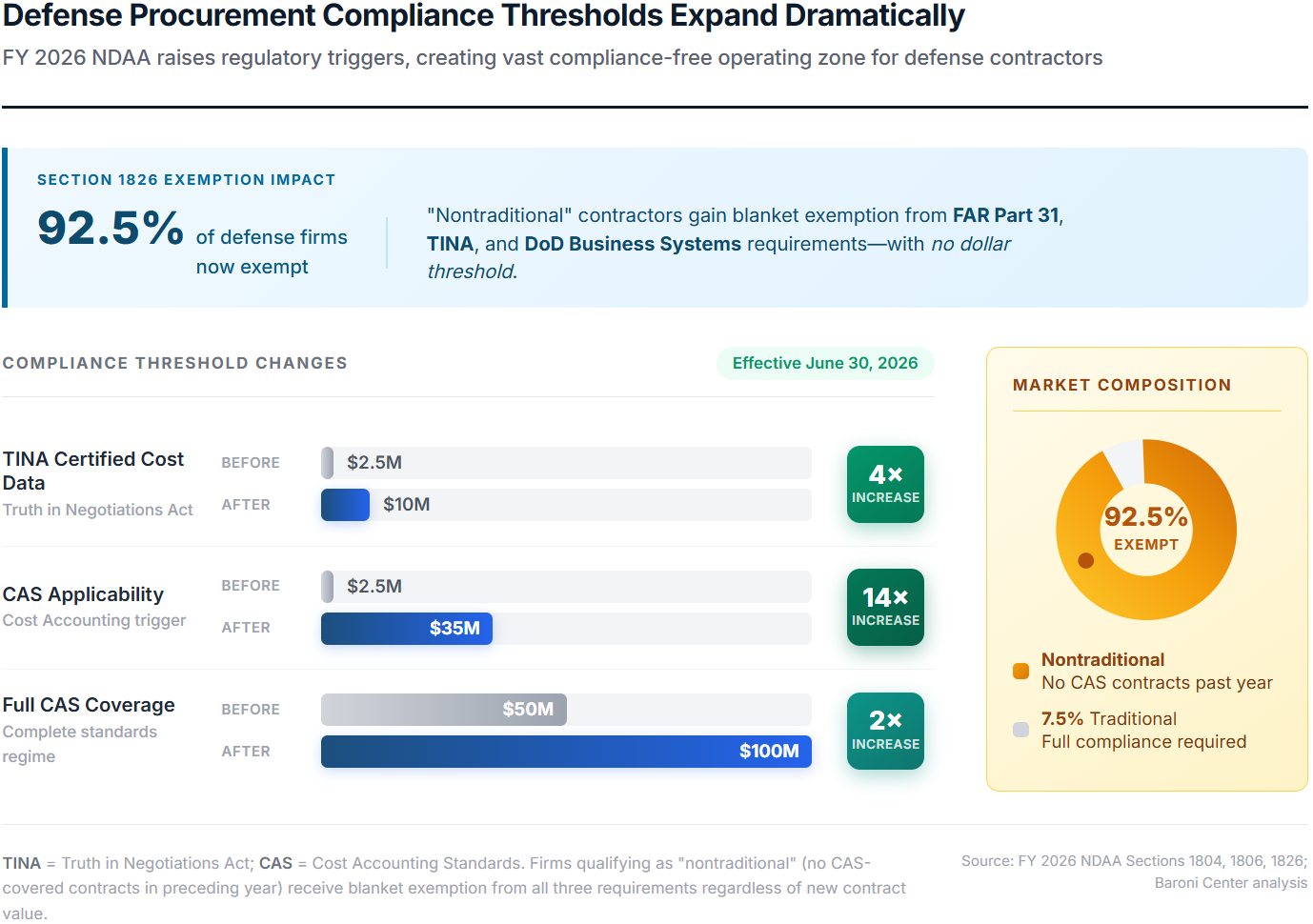

Section 1826 eliminates this moat for 92.5% of potential contractors.

The provision exempts "nontraditional defense contractors"—defined as any entity not currently performing, and not having performed in the preceding year, a contract subject to full Cost Accounting Standards coverage—from three pillars of traditional defense oversight:

The exemption carries no dollar threshold. A nontraditional contractor can now compete for billion-dollar defense programs without building CAS-compliant accounting infrastructure, without submitting certified cost or pricing data, and without undergoing business system audits that can result in payment withholds for deficiencies.

"92.5% of firms in the defense market qualify as nontraditional under the statutory definition—only 7.5% have held full CAS-covered contracts in the past year." — Baroni Center analysis

The legislative package extends beyond Section 1826. Section 1804 raises the TINA threshold from $2.5 million to $10 million, effective June 30, 2026. Section 1806 increases the CAS trigger from $2.5 million to $35 million and full CAS coverage from $50 million to $100 million. Section 1822 strengthens commercial-first mandates, requiring formal market research and written determinations before procuring noncommercial products. Section 1824 prohibits primes from automatically flowing down all DFARS clauses to commercial subcontractors—eliminating a key strategy traditional primes used to shift compliance burdens downstream.

The coordinated policy campaign makes the administration's intent unmistakable. In April 2025, Executive Orders 14265 and 14275 initiated FAR overhaul. In August, a joint memo reformed the requirements process. On November 7, Hegseth declared the old system dead. On December 18, the NDAA codified structural change with bipartisan support. On January 7, the buyback executive order added enforcement pressure. This wasn't reactive—it was a nine-month planned offensive against a procurement system that the Section 809 Panel had already concluded was fundamentally broken.

The market hasn't priced this structural shift because it reads as regulatory arcana. But the implications compound. Palantir's $10 billion Army Enterprise Agreement, announced July 31, 2025, consolidates 75 contracts into a single framework, treating commercially-developed software as COTS (Commercial Off-The-Shelf) products with minimal FAR Part 31 exposure. The Anduril-led NGC2 prototype, awarded via Other Transaction Authority in July 2025, partners Palantir, Microsoft, and smaller contractors to build the Army's next-generation command and control architecture—moving from proof-of-concept to capability validation in twelve months rather than the traditional five-to-seven-year timeline.

In December 2024, the Financial Times reported that Palantir and Anduril are forming a consortium with SpaceX, OpenAI, Scale AI, and Saronic to bid jointly on defense contracts—explicitly positioning as an alternative to traditional primes. Anduril has committed nearly $1 billion of its own capital to Arsenal-1, a hyperscale manufacturing facility in Columbus, Ohio—precisely the kind of self-funded capacity investment the administration demands from contractors. These aren't anomalies. They're templates for how defense acquisition operates under Section 1826.

In early October 2025, Reuters reported that an internal Army memo labeled the NGC2 prototype "very high risk" due to cybersecurity vulnerabilities. The memo, authored by Army Chief Technology Officer Gabriele Chiulli, stated that third-party applications embedded in the system contained hundreds of unassessed vulnerabilities, including one application with 25 high-severity code flaws.

The story reinforced a familiar narrative: Silicon Valley's move-fast-break-things ethos is incompatible with mission-critical military systems. Commercial contractors lack the institutional knowledge, security discipline, and process rigor that traditional defense primes have developed over decades. Speed is the enemy of safety. The Pentagon's romance with tech disruptors will end badly.

This narrative misses what happened next—and misunderstands what the memo actually represents.

The Army continued the NGC2 program. The cybersecurity memo wasn't a failure; it was exactly what agile procurement should look like—identify vulnerabilities early, remediate quickly, iterate forward. In October 2025, the 4th Infantry Division conducted Ivy Sting 2, testing the system's ability to deconflict airspace before firing weapons. Soldiers fired 26 live missions with M777 howitzers, running the new system side-by-side with legacy crews. Army Chief Information Officer Leonel Garciga characterized the memo as part of a normal process for triaging cybersecurity vulnerabilities—issues addressed within weeks, not years. In September 2025, the Army awarded a second NGC2 contract to a Lockheed Martin-led team, explicitly maintaining competition and preserving a traditional-prime fallback while accepting commercial development risk.

The pattern reveals the skeptics' blind spot: DoD leadership has made an institutional decision to shift the risk tolerance curve—accepting higher cyber risk in exchange for faster development cycles and commercial innovation. The Replicator Initiative confirms this isn't a one-off experiment. DoD's effort to field thousands of attritable autonomous systems awarded contracts to more than 35 companies by late 2024, with 75% classified as nontraditional defense contractors who had never held major Pentagon contracts. They're not dismissing the tradeoffs. They're deliberately choosing speed over legacy acquisition timelines.

The administration's rhetoric has been blunt. Army Secretary Dan Driscoll told the TBPN Live podcast in May 2025: "I will measure it as success if in the next two years, one of the primes is no longer in business." He later said primes "conned the American people" into thinking only bespoke military solutions work. Deputy Defense Secretary Steve Feinberg told lawmakers the current acquisition system favors legacy contractors by incorporating "gold-plated" requirements that hold commercial vendors back.

The stock market's reaction to the January 7 executive order tells its own story. Defense primes fell 3-5.5% on the announcement. The next day, after Trump proposed a $1.5 trillion FY 2027 defense budget, Lockheed Martin surged 7% and Northrop Grumman jumped 8%. The selloff reversed completely. Markets concluded that budget growth dominates capital allocation restrictions—at least in aggregate.

But aggregate masks distribution. Traditional primes remain bound by CAS, TINA, DFARS business-systems audits, and FAR Part 31. They face a structural disadvantage when bidding against exempt nontraditional firms with lower compliance costs, faster development cycles, and commercial capital bases that don't depend on government contract financing. The incumbency that once protected them now weighs them down.

Separating signal from noise reveals the structural trap facing traditional primes.

The Trump executive order and Section 1826 create a pincer movement against traditional defense contractors. From above, the administration restricts capital returns—the top four primes returned $89 billion to shareholders through buybacks and dividends from 2021-2024, approximately two-thirds funded by DoD contract cash flows per Semler's analysis cited in Senator Warren's December letter. From below, commercial competitors enter without compliance overhead, competing for software, AI, and sensor programs where commercial technology leads.

Traditional primes can't simply shed their compliance infrastructure. Their existing contracts require it. Their cost structures assume indirect rate recovery. Reducing overhead to compete with exempt contractors means becoming less competitive for remaining FAR-based contracts. Maintaining overhead means accepting margin compression as commercial competitors underprice on simplified acquisitions.

The valuation gap reflects this divergence. As of mid-January 2026, Palantir's market capitalization exceeds $407 billion—approximately three times Lockheed Martin's $135 billion. Markets have priced in a power shift from platform manufacturers to software integrators.

Investment Implications:

The thesis expresses most clearly under specific conditions: sustained implementation of exemption declarations, limited waiver usage, margin pressure appearing in traditional prime guidance, and continued commercial contractor execution on major programs. Under those conditions:

Watchlist — Thematic Exposure: Commercial defense technology with demonstrated government traction. Palantir's $10 billion Army framework provides visibility through 2035, though current valuation (64x EV/Revenue on 2026 estimates) suggests markets have already priced substantial execution. Microsoft's NGC2 partnership creates defense revenue optionality underappreciated in the broader MSFT story. Anduril's anticipated IPO would offer direct exposure to the transition thesis.

Watchlist — Caution: Traditional primes face multiple compression as investors re-rate them from "stable defense oligopoly" to "industrial companies facing commercial disruption." The "too essential to fail" dynamic provides a floor—there's no alternative for F-35 or Columbia-class SSBNs—but software-intensive programs are now contestable. Section 1826 doesn't eliminate all barriers: security clearance requirements, export controls, and programmatic integration risks remain, and DoD retains authority to waive the exemption with congressional notification.

These observations reflect thematic analysis, not security-specific recommendations. Valuation, position sizing, and suitability depend on individual circumstances beyond the scope of this commentary.

Constraints are real. The EO's authority to regulate corporate financial decisions is unprecedented—federal intrusion into capital allocation at this scale has no direct precedent—and may face legal challenge. Congressional appropriators resist portfolio reforms; the Army's "Agile Portfolio Management" was rejected in FY2026 appropriations. But even partial implementation shifts the landscape materially.

The catalyst timeline is compressed: February 6 brings the Secretary's underperformer list. June 30 marks the TINA threshold increase. By Q1 2027, the competitive landscape will look materially different than consensus expects.

Legislative change of this magnitude occurs rarely—the last comparable defense acquisition reform was the Federal Acquisition Streamlining Act of 1994. Section 1826 is self-executing and bipartisan; it requires no appropriations, no implementation guidance, and no executive discretion to take effect. The compliance moat has already fallen for 92.5% of potential contractors. The executive order adds near-term pressure on capital returns but faces legal uncertainty—the legislative foundation does not. Congressional appropriators may resist portfolio management reforms, but the compliance exemptions are law. The 0.8-point discount from 10.0 reflects transition timing uncertainty: how quickly commercial contractors scale, how aggressively DoD uses exemption declarations, and whether traditional primes can adapt faster than expected. Direction is high conviction; velocity is the variable.

This commentary is provided for informational purposes only and does not constitute investment advice, an offer to sell, or a solicitation to buy any security. The information presented represents the opinions of The Stanley Laman Group as of the date of publication and is subject to change without notice.

The securities, strategies, and investment themes discussed may not be suitable for all investors. Investors should conduct their own research and due diligence and should seek the advice of a qualified investment advisor before making any investment decisions. The Stanley Laman Group and its affiliates may hold positions in securities mentioned in this commentary.

Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal. Forward-looking statements, projections, and hypothetical scenarios are inherently uncertain and actual results may differ materially from expectations.

The information contained herein is believed to be accurate but is not guaranteed. Sources are cited where appropriate, but The Stanley Laman Group makes no representation as to the accuracy or completeness of third-party information.

This material may not be reproduced or distributed without the express written consent of The Stanley Laman Group.

© 2025 The Stanley-Laman Group, Ltd. All rights reserved.

SLG is an independent investment management and advisory firm serving ultra-high-net-worth individuals, families, and institutions.