When Hammond Power Solutions reported Q3 2025 results on October 23, the headline numbers were solid: $218 million in revenue, 13.7% year-over-year growth, the company's second-highest shipment quarter in its 108-year history. The real story came in CEO Adrian Thomas's prepared remarks: substantial orders received shortly after quarter-close amounting to 53% of the Q3 closing backlog. Management attributed the surge primarily to data center projects.

Let that figure settle. In a matter of weeks following quarter-end, Hammond booked orders equivalent to more than half its existing backlog — driven substantially by data center demand. These orders will ship primarily in 2026 from new facilities in Mexico, which are being reconfigured with additional equipment to support the volume. The company is simultaneously expanding its Monterrey facilities to add approximately $100 million of annual production capacity to meet demand it already has visibility into.

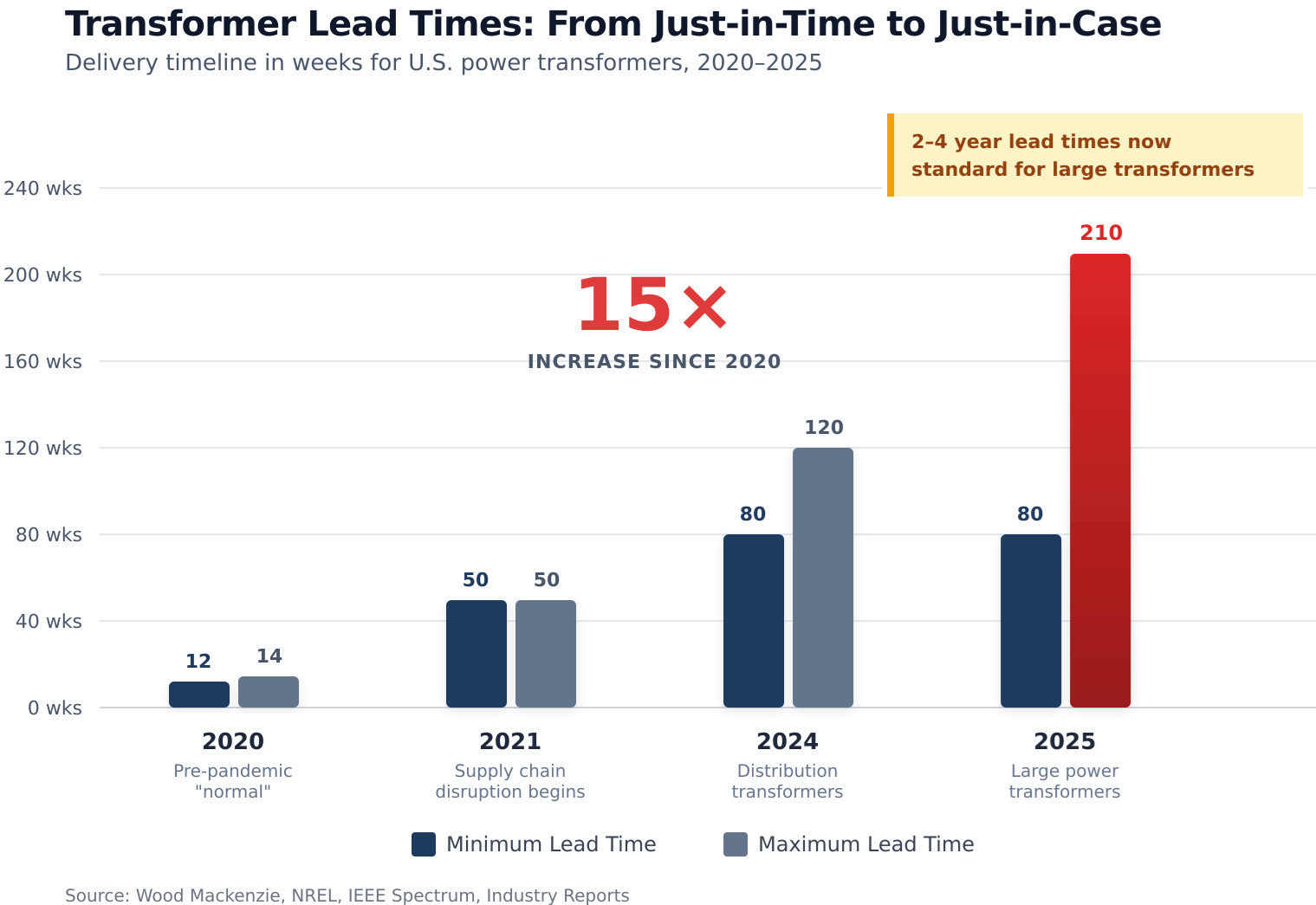

Hammond manufactures dry-type transformers — the category required for indoor installation where fire safety is paramount. Every data center needs dozens of these units to step voltage down within the facility. While large power transformer lead times have stretched to 80-210 weeks at the grid interconnection, dry-type transformers face their own acute shortage. Wood Mackenzie reports lead times have doubled from 50 weeks in 2021 to nearly two years. Prices have increased over 60% in the same period

The shortage compounds at every level. U.S. transformer demand has surged 116% since 2019 for power transformers and 41% for distribution transformers, according to Wood Mackenzie's analysis released in August 2025. The consulting firm projects a 30% supply shortfall for power transformers and 6-10% for distribution transformers in 2025 — forcing utilities to rely on imports for 80% of large transformer supply and 50% of distribution units.

What makes Hammond's position exceptional is not just demand visibility, but supply chain integration. The company manufactures across facilities in Canada, the United States, Mexico, and India, with expansion capacity already under construction. In a market defined by multi-year backlogs and constrained supply, Hammond has both the orders and the capacity roadmap to capture them.

The supply chain vulnerability extends to raw materials. Grain-oriented electrical steel — the specialized iron-silicon alloy that forms transformer cores — has become a strategic chokepoint. Thyssenkrupp's December 11 announcement that it would shut German and French GOES production through year-end, with the Isbergues facility operating at 50% capacity for at least four months, represents Europe's capitulation to Asian dumping. GOES imports to Europe have tripled since 2022 and risen another 50% in 2025 alone, priced below European production costs.

The United States faces an even starker reality: Cleveland-Cliffs operates the only domestic GOES production facility, at Butler Works in Pennsylvania. In October 2025, the Defense Logistics Agency awarded Cliffs a five-year, $400 million contract to supply up to 53,000 short tons of GOES — a national security stockpile acknowledgment that transformer steel has become strategic material. Notably, Cliffs cancelled its planned $150 million transformer manufacturing plant in Weirton, West Virginia, in May 2025, after a prospective partner backed out — a decision that underscores how technically demanding and capital-intensive transformer manufacturing remains. Even the sole domestic steel producer couldn't make the vertical integration economics work, validating the competitive moat enjoyed by established manufacturers like Hammond.

The data center demand wave driving Hammond's backlog surge reflects structural electricity growth the grid was not designed to accommodate. The International Energy Agency projects global data center electricity consumption will double to 945 TWh by 2030, with the United States accounting for 240 TWh of that increase — a 130% jump from 2024 levels. S&P Global forecasts U.S. data center grid-power demand will rise 22% in 2025 alone and nearly triple by 2030, reaching 134 gigawatts. Goldman Sachs estimates approximately $720 billion of grid spending will be required through 2030.

Grid interconnection queues now exceed five years in many regions. However, Lawrence Berkeley National Laboratory data suggests only 19% of interconnection queue projects ultimately become operational, with 70% withdrawing. This forces data center operators toward behind-the-meter solutions that require their own transformer infrastructure. Every megawatt of new AI compute capacity requires transformer infrastructure at multiple voltage levels — from utility interconnection down to server rack distribution.

Hammond's 53% post-quarter backlog surge isn't an anomaly. It's the first visible signal of capital flowing toward a constraint that will define infrastructure deployment for the remainder of the decade.

Walk into any infrastructure investor presentation and the conversation centers on generation: natural gas turbines (sold out through end of decade), nuclear restarts (Three Mile Island, Palisades), small modular reactors (2030s at earliest). Ask about transformers and you'll get a puzzled look. Transformers are assumed to be commodity infrastructure — unglamorous, available, someone else's problem.

This assumption persists because transformers have been reliably available for decades. When a utility needed a distribution transformer, lead times averaged three months. The specialized supply chain hummed invisibly, delivering equipment as needed without strategic consideration. The mental model that transformers are commoditized and fungible remains embedded in capital allocation frameworks even as physical reality has diverged.

The market has begun recognizing transformer exposure but continues to misprice its structural nature. Hammond's 156% 52-week return and TSX30 recognition signal growing awareness, yet the thesis remains misunderstood as cyclical rather than structural. First, transformers still lack the narrative appeal of energy transition themes. Solar panels, batteries, wind turbines, and nuclear plants all carry stories about decarbonization and technological progress. Transformers carry electricity from Point A to Point B — essential but unromantic. Second, the companies manufacturing transformers are often small, Canadian-listed, or embedded within diversified industrials. Hammond Power Solutions trades on the Toronto Stock Exchange with a market capitalization around C$2 billion. It doesn't appear in the ETFs or indexes that drive passive capital flows. For investors seeking U.S.-listed exposure, Powell Industries (NASDAQ: POWL) offers an alternative vehicle with similar themes, though less pure-play transformer focus.

Third, and most importantly, investors conflate lead time constraints with demand destruction. When semiconductor shortages emerged in 2021, the response was "demand will be deferred." When transformer shortages emerged in 2022, the assumption was identical. But transformer demand doesn't defer — it accumulates. Every delayed housing development, every data center waiting for grid connection, every utility deferring storm-damaged equipment replacement adds to backlog rather than disappearing.

The Thyssenkrupp shutdown crystallizes the strategic dimension. Europe's largest GOES producer shuttering facilities doesn't create temporary supply constraint — it concentrates global transformer steel production further into Asia (primarily China's Baowu, South Korea's POSCO, and Japan's Nippon Steel) and leaves the United States dependent on a single domestic supplier. When Cleveland-Cliffs abandoned its Weirton transformer plant — despite $50 million in West Virginia state incentives — it demonstrated that even vertically integrated steel producers cannot easily replicate transformer manufacturing expertise. The technical barriers to entry remain formidable.

Hammond Power Solutions has returned over 2,000% over the past five years versus 79% for the TSX Composite. Yet sell-side coverage remains thin — five to seven analysts — and institutional ownership lacks the density typical of industrial leaders. The stock trades at roughly 25-26x trailing earnings, a premium to some industrials but defensible given the growth trajectory and capacity expansion now underway.

The market continues to price transformers as if they were commodity products with elastic supply, ignoring multi-year backlogs, strategic material dependencies, and the structural electricity demand surge that has barely begun. This isn't analytical disagreement about growth rates. It's categorical misunderstanding of where the bottleneck actually sits in the electrification value chain.

Hammond Power Solutions sits at the intersection of multiple secular tailwinds. Data center construction drives custom transformer demand. Grid modernization replaces aging equipment (average large power transformer age: 38 years, often at or beyond design life). Reshoring and industrial policy require electrical infrastructure buildout. Renewable integration demands grid-edge transformation capacity. Each driver independently supports demand growth; together they create the backlog acceleration Hammond just demonstrated.

The Thyssenkrupp closure is not a one-week story. European GOES production operating at reduced capacity through at least April 2026 constrains global transformer manufacturing throughout the period — precisely when North American demand is accelerating. Cleveland-Cliffs' strategic positioning as sole U.S. GOES producer, now with DOD supply contracts, signals government recognition that transformer supply chains have become national security infrastructure.

For investors seeking electrification exposure beyond the obvious generation plays, Hammond offers direct leverage to a constraint the market has not correctly priced. The company has the orders (53% post-quarter backlog surge), the capacity roadmap (Mexico facility expansion, Monterrey additions), and the end-market exposure (data centers driving the backlog surge) to convert structural shortage into sustained earnings growth. The 25-26x trailing multiple reflects some recognition but not the multi-year duration of the supply-demand imbalance. As interconnection queues extend and transformer delivery determines project timelines, capital allocation will follow.

Hammond Power Solutions' 53% post-quarter backlog surge represents the clearest capital-allocation signal available in the transformer supply chain. The company isn't projecting future demand — it has booked orders equivalent to more than half its existing backlog, in weeks, from data center customers targeting 2026 delivery. The Thyssenkrupp GOES shutdown announced December 11 adds acute supply-side constraint to already-structural shortage dynamics. With transformer lead times at 80-210 weeks, prices up 60%+ since 2020, and U.S. supply shortfalls projected at 30% for power transformers, the fundamental thesis is validated by observable market data rather than forecasts.

Rating adjusted to 9.1 (from initial 9.5) based on Council validation that: (1) gross margin compression of 370 basis points year-over-year (30.1% vs 33.8%) with 233 bps attributable to Mexico facility ramp creates meaningful near-term execution risk; (2) the stock's 156% 52-week return and 25-26x P/E indicate considerable optimism already embedded; (3) customer concentration in data centers creates binary risk if hyperscaler capex cycles slow.

This commentary is provided for informational purposes only and does not constitute investment advice, an offer to sell, or a solicitation to buy any security. The information presented represents the opinions of The Stanley Laman Group as of the date of publication and is subject to change without notice.

The securities, strategies, and investment themes discussed may not be suitable for all investors. Investors should conduct their own research and due diligence and should seek the advice of a qualified investment advisor before making any investment decisions. The Stanley Laman Group and its affiliates may hold positions in securities mentioned in this commentary.

Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal. Forward-looking statements, projections, and hypothetical scenarios are inherently uncertain and actual results may differ materially from expectations.

The information contained herein is believed to be accurate but is not guaranteed. Sources are cited where appropriate, but The Stanley Laman Group makes no representation as to the accuracy or completeness of third-party information.

This material may not be reproduced or distributed without the express written consent of The Stanley Laman Group.

© 2025 The Stanley-Laman Group, Ltd. All rights reserved.

SLG is an independent investment management and advisory firm serving ultra-high-net-worth individuals, families, and institutions.